We have identified a more suitable language of this document. To change language to please click here or close

We have identified a more suitable language of this document. To change language to please click here or close

For storing your preferred CMS location, analysing referrals from LinkedIn and embedding third party content we need your consent (which you can withdraw any time).

This website uses cookies so that we can provide you with the best user experience possible. Our Cookie Notice is part of our Privacy Policy and explains in detail how and why we use cookies. To take full advantage of our website, we recommend that you click on “Accept All”. You can change these settings at any time via the button “Update Cookie Preferences” in our Cookie Notice.

Technical cookies (required)

Technical cookies are required for the site to function properly, to be legally compliant and secure. Session cookies only last for the duration of your visit and are deleted from your device when you close your internet browser. Persistent cookies, however, remain and continue functioning on repeat visits.

Analytics

CMS does not use any cookie based Analytics or tracking on our websites; see details here.

Personalisation cookies

Personalisation cookies collect information about your website browsing habits and offer you a personalised user experience based on past visits, your location or browser settings. They also allow you to log in to personalised areas and to access third party tools that may be embedded in our website. Some functionality will not work if you don’t accept these cookies.

Social media cookies

Social Media cookies collect information about you sharing information from our website via social media tools, or analytics to understand your browsing between social media tools or our Social Media campaigns and our own websites. We do this to optimise the mix of channels to provide you with our content. Details concerning the tools in use are in our privacy policy.

CMS Expert Guide to electric vehicle regulation and law

Interest in EVs has waxed and waned over the years, but the last ten years have seen a momentous surge in the market, which is set to transform the automotive industry.

The International Energy Agency (“IEA”) has examined this market growth in its recent report entitled “Global EV Outlook 2017: Two million and counting”.

1

Global EV Outlook 2017 (accessed 15 February 2018)

The IEA cites the following headline statistics:

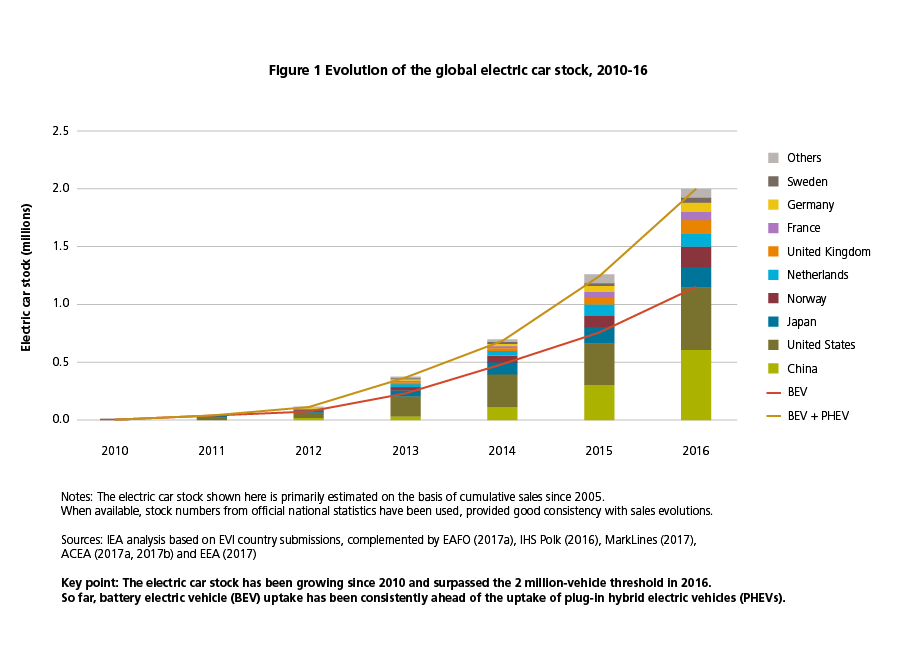

The number of electric cars on the road globally surpassed 2 million in 2016, having reached 1m in 2015. A stark increase from 2005, when the figure was just over 1,000. China and the US account for more than half of electric cars in the world.

A new record of sales of EVs was achieved in 2016, with over 750,000 sales worldwide.

China was by far the largest market in 2016, accounting for almost half of the EV sales in 2016. This was more than double the number of registrations in the US, the second largest market.

In terms of market share, Norway is incontestably the global leader with 29% of its total passenger light duty vehicle (“PLDV”) sales in 2016 being registered as EVs. China’s vast EV stock constitutes only 1.5% of its total PLDV sales. These were two of only six countries to achieve an electric car market share of above 1% of their total PLDV sales.

However, there has been a slowdown in market growth rates in recent years which has been linked to the removal of government subsidies. Whilst it was expected that, in-line with all emerging markets, growth rates would ultimately inevitably decline, the EV market still seems a million miles away from the potential scale it could achieve, with EVs representing just 0.2% of the total number of PLDVs in circulation globally

2

As above in fn. 1

.

Drivers of EV market growth

Tackling climate change

Global framework Climate change is a significant driver in the development of EVs. The Paris Agreement, which came into force in November 2016, brings a large number of nations together in the pursuit of reducing greenhouse gas (“GHG”) emissions and limiting global warming to well below 2°C. The Agreement requires all parties to declare “nationally determined contributions” (“NDCs”), which embody efforts by each country to reduce national emissions and adapt to the impacts of climate change.

EVs have the potential to be instrumental in enabling countries to meet their NDC targets. Electric motors are more efficient than combustion engines and this, coupled with the transition to a lower-carbon electricity generation mix, is how EVs can contribute to the reduction of carbon emissions. The 2015 Paris Declaration on Electro-Mobility and Climate Change states that transport contributes to 23% of the current global energy-related GHG emissions and is growing faster than any other energy end-use sector. The IEA has estimated that EVs must represent 35% of new vehicle sales by 2035 to limit climate change to less than 2%. This is recognised and demonstrated in the EU’s transport-related measures outlined below, which have been put in place to help the EU achieve its NDC goals of reducing GHG emissions by 40% below 1990 levels by 2030 and 80% below 1990 levels by 2050

3

See the Commission Staff Working Paper at the link below for a detailed summary of the existing EU measures on sustainable transportation.

Comission Staff Working Document

:

The 2009 Renewable Energy Directive requires member states to ensure that at least 10% of transport energy consumption is derived from renewable sources by 2020.

The 2009 Emission Performance Standards Regulation requires car manufacturers to achieve a certain average emissions level across the new vehicles they sell and to make available to consumers information about the emission performance of their vehicles.

The 2009 Clean Vehicles Directive requires public bodies in Member States to consider fuel consumption and pollutants when procuring road vehicles.

The European Commission’s 2011 Single European Transport Area white paper sets a target of a 60% reduction in transport GHG emissions by 2050 (by 1990 levels).

The 2014 Alternative Fuels Infrastructure Directive requires member states to put in place national policy frameworks for the development of the market for non-fossil fuels in the transport sector, including the provision of adequate EV charging infrastructure in developed areas.

The European Commission’s 2016 Strategy for Low-Emission Mobility summarises at a high level its focuses for legislative development and the application of support funding in relation to the transition to sustainable transportation. Such focuses include the efficiency of taxation and price signals, the evolution of emission performance standards and the improvement of vehicle emissions testing to regain consumer trust.

Building on this, more rigorous vehicle emissions testing standards, including testing in real driving conditions, were imposed in September 2017; in November 2017, the Commission proposed a 30% reduction of the EU’s mandatory average emissions levels for manufacturers of light vehicles by 2030.

4

Proposal for post-2020 CO2 targets for cars and vans

The NDCs of other major polluting nations demonstrate varying levels of ambition: China has committed to a 60% reduction in GHG emissions from 2005 levels by 2030, whereas India is targeting 33%, and Russia is aiming for a 25% reduction in GHG emissions from 1990 levels by 2030. The US has formally notified the UN of its intention to withdraw from the Paris Agreement, but the target it had previously set was a 26% reduction in GHG emissions from 2005 levels by 2025. China, India, Japan and the US (unlike the EU) included specific transport emissions measures in their NDCs, including fuel efficiency improvements and alternative fuel promotion.

The Bloomberg New Energy Finance report – Electric Vehicle Outlook 2017 predicts that by 2040 EVs will displace million barrels of transport fuel per day, and add 5% to global electricity consumption.

Local policy implications This global-level ambition to reduce emissions has trickled down to national-level government policies and initiatives. These have ranged from:

In 2009, the IEA’s Clean Energy Ministers set up the Electric Vehicle Initiative dedicated to accelerating the deployment of EVs worldwide. Its EV30@30 campaign launched in 2017 sets a collective “aspirational goal” for EV1 members of a 30% market share for EVs by 2030.

5

Proposal for post-2020 CO2 targets for cars and vans

Measures that encourage take up of EVs in large cities (e.g. Paris, London, Mexico City, Stuttgart, Tokyo) including the banning or restricting of polluting vehicles, or imposing charges for such vehicles, entering specified city zones.

Financial incentives for the purchase of new EVs, along with a range of tax and access benefits for ownership, across larger European economies. Norway and the Netherlands are leading the way on incentives, with special measures including nationwide toll exemptions in Norway and an urban charging point development regime led by resident applications in Amsterdam.

The tightening of vehicle emissions standards. The EU is currently ahead of the rest in this respect, but the US and Canada are phasing in even more stringent standards. The standards in China and India are less demanding, though plans are in place in both jurisdictions to catch up to the EU.

China’s remarkable EV sales growth is largely attributable to promotional measures such as sizeable purchase subsidies, large-scale charging infrastructure funding and restrictions on registrations of combustion-engine vehicles. However, the market is already showing signs of over-reliance on subsidies, with a precipitous fall in sales linked to subsidy reductions in early 2017.

Consumer demand

Demand for electric vehicles is increasing due to factors including the following:

Increasing affordability At present, EVs are generally more expensive to purchase than their conventionally powered counterparts, but the gap is closing. In May 2017, the Financial Times (“FT”) reported on a UBS analysis that forecast cost parity between EVs and conventional gas and diesel vehicles as early as 2018 in Europe, by 2023 in China and by 2025 in the US.

9

Electric car costs forecast to hit parity with petrol vehicles

In September 2017, the Bloomberg New Energy finance research that predicted “tumbling battery prices” would make EVs cheaper to buy than conventional vehicles in most countries by 2025–29, predicting that EVs would make more than half of new car sales worldwide by 2040.

10

Energy executives confident over renewables future: https://www.ft.com/content/fbbc05b0-9c75-11e7-8cd4-932067fbf946 and cf Nissan’s recent prediction of 2025 cost parity: https://www.ft.com/content/7bbd9a9a-1326-11e8-940e-08320fc2a277

Consumers are also attracted by the comparative cheapness of EVs to run and maintain: while the price of diesel and petrol continue to increase, the cost of charging an electric car is negligible by comparison; EVs contain many fewer moving parts than combustion-engine vehicles.

The release of the Toyota Prius in Japan in 1997 and worldwide in 2000 which became the world’s first mass-produced (and subsequently best-selling) hybrid EV;

The announcement by Tesla in 2006 that it was starting production of luxury electric sports cars that could go more than 200 miles on a single charge following in 2017 with the launch of Tesla’s first mass-market model.

Spurred by Tesla’s first announcement, other automakers have begun rolling out their own EV models and it is reported that today there are now 23 plug-in electric and 36 hybrid models available. In 2017, many of the world’s largest automakers (including VW, Volvo, Toyota, General Motors, Renault-Nissan and Ford) announced ambitious targets for investment in and sale of electric models. Amongst these, Volvo, announced that every new car in its range would have an electric power train available from 2019.

Climate change is also ever-present in the headlines.

Challenges

While deployment of EVs could alleviate a number of environmental concerns, mass uptake and market saturation will bring with it its own set of challenges. Cost is also a significant issue.

Cost

EVs are heavily subsidised in many countries and whilst these subsidies are crucial to the success of a mass EV rollout they may not be liable in the long-term. The Bloomberg New Energy Finance report forecasts that EVs will become price competitive without reliance on subsidies by 2025.

Charging infrastructure

Range anxiety is one of consumers’ key fears when considering switching to an EV. Charging infrastructure will need to keep pace with the growing number of EVs. Businesses across electricity markets will need to take into account the impact of the additional capacity required from each country’s grid. A rapid increase in demand for electricity from the grid is not a foregone conclusion; it is possible that demand from the grid could decrease as businesses and domestic consumers forge their own charging solutions, whether by means of embedded generation or energy storage.

Batteries

Batteries have been a significant obstacle in the wider deployment of EVs to date and represent a large proportion of their cost. Battery characteristics including energy density, longevity and charge time impact greatly on the range and performance of EVs. Manufacturers have made significant improvements in these areas, but there is still a way to go to achieve value parity with vehicles with combustion engines, especially for heavier vehicles.

The table below sets out the types of batteries currently used in EVs:

Battery type

Description and use

Advantages

Disadvantages

Lead-acid batteries

Commonly used in forklifts and golf carts. Rarely used in modern EVs.

Cheap to produce

Toxic

Volatile

Short lifespan

Low energy density

Nickel metal hydride [NiMH]

Uses hydrogen ions to store energy around nickel and e.g. titanium. Currently used primarily in hybrids but rarely in BEVs.

Safer than Li-ion –fewer volatile materials.

Faster rate of self-discharge when not in use than Li-ion.

Semi-toxic – requires special handling to recycle.

Recharging early candiminish capacity.

Lithium ion batteries [Li-ion]

Uses liquid electrolyte. Currently considered to have the most potential for mass- market EVs.

Higher energy density than NiMH.

Versatile – greater scope for varyingdischarge currents, voltages, charge times etc.

High cost – especiallythe most advancedunits.

Degrades with age atfaster rate thanNiMH.

Technology may havereached an energydensity barrier.

Despite the various problems with current battery technologies, automakers have largely, so far, eschewed hydrogen fuel cells. Compared to batteries, fuel cells would have the benefits of being smaller, lighter and instantly rechargeable; but they are currently much further from economic viability than batteries. Instead, new battery types are in development, with both “solid state” and “lithium air” batteries promising further gains in the crucial variable of energy density.

Policy, regulation and other legal issues

As previously indicated, the EV market is heavily reliant on policy support in respect of both EVs and charging infrastructure. Policy tools currently in use include purchase subsidies, research, development and deployment measures, fuel economy standards, mandates for automakers to sell a set portion of zero-emission vehicles, and access restrictions. It is thought that policy support will remain indispensable, at least in the medium term; however, as EVs become more cost competitive and economics takes the driving-seat, policy adjustments may be required.

Cohesive regulatory frameworks for EVs are not yet well-established. To prepare for the universal electrification of roads, there is likely to be a need for national legislation on a broad range of issues, including vehicle licensing and taxation, vehicle and charging standards and the smart management of grid demand.

Opportunities

The increase in deployment of EVs creates a wealth of opportunities for investors, automotive manufacturers, electricity generators, supply chains, network operators, energy suppliers, consumers, infrastructure owners and developers, real estate developers and other electricity and automotive sector participants. In fact, the market potential is drawing in participants from other sectors too, including UK technology company Dyson, which has recently announced its £2 billion project to develop and build EVs from scratch, which it claims will bring more inventive designs to the market.

12

Dyson bets on electric cars to shake up industry

This is a truly exiting space driving innovation.

About this guide

The CMS Energy group is passionate about developments that impact the EV industry. We strive to constantly be on top of R&D, engage in constructive dialogue and help our clients manage the challenges and opportunities brought by change. This Expert Guide is our approach to help our clients, whether they are battery or vehicle manufacturers, EV infrastructure providers, network or supply businesses, get acquainted with EV developments across the world. We started with a chapter on developments in the UK and continue to update this guide monthly with chapters from other jurisdictions across Europe, Asia, the Middle East and Latin America.

How we can help

Please contact your CMS contact in the relevant jurisdiction if you wish to discuss the impact of these changes for your business further or for more general enquiries please contact us.

Glossary of EV terms

AC Motor: an electric motor driven by an alternating current.

BEV: Battery Electric Vehicle: EVs that use electric motors powered by on-board batteries.

DC Motor: a rotary electrical motor that converts direct current electrical energy into mechanical energy.

EV: Electric Vehicle: uses one or more electric motors or traction motors for propulsion.

EVI: Electric Vehicles Initiative: a multi-governmental policy forum established in 2008 dedicated to accelerating the deployments of EVs worldwide. Members: Canada, China, France, Germany, Japan, the Netherlands, Norway, Sweden, the UK and the US.

GHG: greenhouse gas: a gas that contributes to the greenhouse effect by absorbing infrared radiation. Carbon dioxide and chlorofluorocarbons are examples of greenhouse gases.

HEV: Hybrid Electric Vehicle: combine a normal petrol or diesel engine with an electric motor – rely on combustion and electric propulsion fairly evenly.

ICE: Internal Combustion Engine: an engine which generates motive power by the burning of petrol, oil, or other fuel with air inside the engine, the hot gases produced being used to drive a piston or do other work as they expand.

IEA: International Energy Agency: an autonomous organisation which works to ensure reliable, affordable and clean energy for its 29 member countries and beyond.

NOC: Nationally Determined Contributions: a term used under the United Nations Framework Convention on Climate Change (UNFCCC) for reductions in greenhouse gas emissions that all countries that signed the UNFCCC were asked to publish in the lead up to the 2015 United Nations Climate Change Conference.

Paris Agreement: an agreement within the United Nations Framework Convention on Climate Change dealing with greenhouse gas emissions mitigation, adaptation and finance starting in the year 2020.

PEV: Plug-in Electric Vehicle: can be recharged from any external source of electricity and the electricity stored in the rechargeable battery packs drives or contributes to drive the wheels.

PHEV: Plug-in Hybrid Electric Vehicles: have a larger battery and fall back on a smaller combustion engine less frequently than a HEV.

PLDV: passenger light-duty vehicle.

R&D: Research and Development.

ULEV: Ultra-Low Emission Vehicle: a vehicle that emits extremely low levels of emissions compared to others. In some jurisdictions it is defined in law and may be given tax or other advantages, or avoid restrictions or taxations imposed on high emission vehicles.

Social Media cookies collect information about you sharing information from our website via social media tools, or analytics to understand your browsing between social media tools or our Social Media campaigns and our own websites. We do this to optimise the mix of channels to provide you with our content. Details concerning the tools in use are in our privacy policy.